I bought my first life insurance policy in 2007. It took me about 3 months to finalise which policy to buy. I took my time to research and to select the right policy.

Now, I bought insurance because I wanted “insurance”, a protection against a risk, the risk that how would my family take care of itself financially if I evaporate from this planet.

And that’s what insurance is ‘bought‘ for.

Actually, I was wrong. I found it surprising then, and even today, that people don’t ‘buy‘ insurance. They get ‘sold‘ insurance. Why?

Why do you get ‘sold’ insurance?

Call it the case of perverse incentives and lack of understanding of insurance as a financial tool.

Most insurance policies get ‘sold’ because they provide certain tax benefit under Section 80C of the Income Tax Act. I don’t think all the insurance that is sold would be sold without this one incentive.

Then comes the add-on of earning returns on the insurance investment. You see, the most sold insurance policies are actually investment plans in the guise of insurance. You would never take up an insurance policy that does not return you anything. At least that’s what the popular belief is.

As an investment consultant, I have had the opportunity to interact with hundreds of investor clients. As part of building their financial plans, I used to evaluate their insurance policies too.

I realised that almost all had an insignificant amount of insurance coverage. This was because, most had been sold investment-based plans with very little insurance component to speak of. Frankly, for their income levels and lifestyle, the cover was grossly inadequate.

They were saddled with endowments, money back, Unit linked Insurance Plans (ULIPs), whole life plans and what not. Such policies fail to serve the core purpose of insurance because most of the premium money was channelised towards investments and not providing the desired insurance cover.

Take this case of one of my clients. While his actual insurance cover requirement was Rs. 2 crores, he had just Rs. 10 lacs of insurance cover. And he was paying a premium of a whopping Rs. 2 lacs per year. Shocking!

Actually, for a person of age 35 years, a Rs. 1 crore insurance cover in a 30 year policy would cost only Rs. 12,000 to Rs. 15,000 per year.

That brings us to the other point – lack of awareness of insurance as a financial tool.

As I said, most people don’t buy life insurance for its “takes care of dependents in case of loss of life of the earning member” benefit. They don’t understand that having the right amount of insurance cover can give their dependents, their family adequate financial protection and a worry free financial future. At least till the time your wealth grows enough to take care of all financial needs of the family, even in your absence.

Taking my example further, if ‘my body were to expire‘, my family should receive enough money to take care of their financial needs. That’s what my insurance should do for me.

But you see, even after paying a hefty insurance premium, why don’t we get adequate insurance cover?

That brings me to the big mystery of the insurance premium.

Have you ever wondered what is the insurance premium utilised for?

What is the break up of this insurance premium that you pay regularly? Where does the money go?

Let’s demystify premium and understand it in a little more detail.

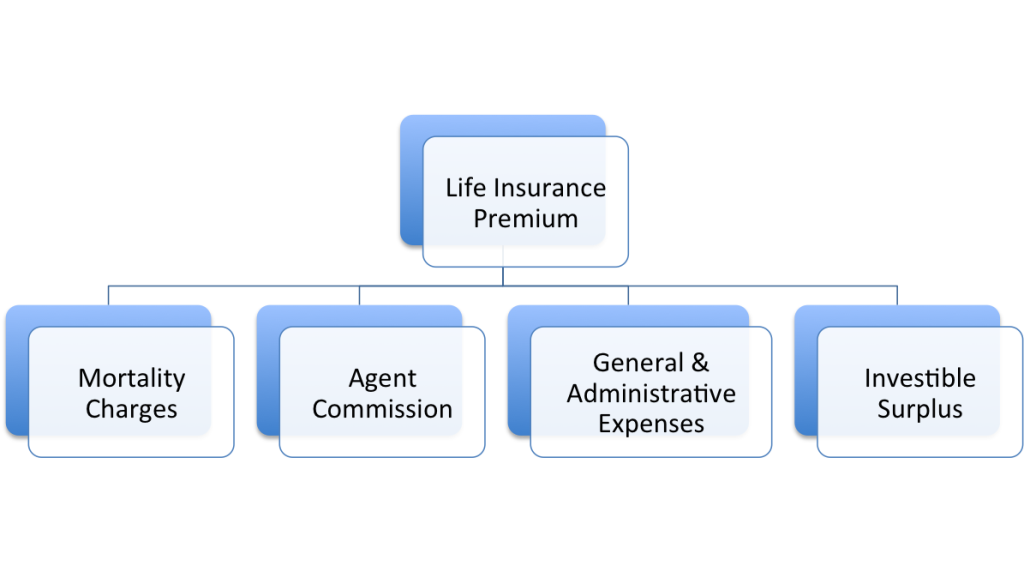

Demystifying the life insurance premium

Your life insurance premium typically comprises of the following:

- Mortality Charges

- Agent Commission

- General & Administrative Expenses (including fund management charges)

- Investible Surplus

- Mortality Charges sit at the core of the insurance coverage. They are based on the amount of insurance cover that you take. It is also known as Sum Assured. The amount that your dependents will receive in case you stop breathing forever. The higher the cover opted for, the higher will be this charge.

-

Agent Commission is pretty straightforward. If you have bought your policy from an agent, this is the commission paid to the agent. Of course, it comes out from the money you pay to the company. It is typically higher for investment-based policies and not for pure insurance policies like term plans. That is one more reason that your banker or your agent will not sell you a pure term plan. It doesn’t benefit him as much. You can also avoid this charge, if you buy online directly from the insurance company.

-

General & Administration expenses take care of the running of the insurance company, which operates the policy for you. It will cover all the expenses it has to bear to remain in operation and serve the claims as and when they become due. For investment-based policies, the fund management charges are also part of this expense head.

- Finally, what is left of the above is then called the Investible Surplus. It is the money which is then further invested into various securities to generate a return which is then given back to you. Investment like government securities form a part of endowment and money back plans’ investments while ULIPs tend to invest a substantial part of their money in stocks.

Why don’t you buy pure life insurance?

Because, you feel there is no point wasting money in a term plan – the pure insurance plan. If nothing happens to you, the money just goes down the drain. There is no return. Hence, you believe that an investment-based policy will at least get you back your investment along with some return.

A big big fallacy this is. As explained in the insurance breakup, when you buy pure insurance, you are paying for mortality charges, general and admin expenses, and some agent commission, of course. When you take up an investment-based insurance, you are adding upto all the 4 heads as shown in the breakup. All this contribution is going out of the premium you pay to the insurance company.

So, what should you do?

First and foremost, it is important to get the right insurance cover in terms of Sum Assured. The smart person would choose insurance for this sake and hence take up a pure term plan. One can go for the cheapest plan from a reliable company. I personally have an HDFC Click to Protect Online Policy and a Term plan from Max Insurance. I am sure there are others in the market which offer the best quote to you for your need.

Next, if you have any other policy apart from the one that offers you only insurance, it is time to do away with it. The bottomline is don’t confuse insurance and investment. Both have a separate place in your financial life.

This is what I also advised my client who was giving away Rs. 2 lacs per year in insurance premium. He is glad he followed it then.

Between you and me: My personal life insurance cover is Rs. 1 crore. What is yours? Have you too been tricked into buying investment plans in the name of insurance? Do share your experiences in the comment, for the benefit of others.