“Vipin, I am planning to start investing in mutual funds. However, I do not want to go headlong into equity so will start with a balanced fund.”

OK. That sounds good. Balanced funds bring the best of both the worlds to you.

“Now, I was told about one of the most reputed funds – HDFC Prudence. But then I realise that HDFC has another fund – HDFC Balanced. I am confused.”

Why are you confused Vinay?

“Arre bhai! Which one should I invest in? And why are there 2 balanced funds in the same fund house?”

OK, lets begin from the start. What were you told about HDFC Prudence Fund?

“That it has a good track record. Also, that is managed by one Mr. Prashant Jain, who is supposedly one of the best fund managers.”

Hm, anything else?

“I also looked up the site which gives star ratings. It has got 4 stars.”

We both smiled.

“I know it doesn’t matter. OK, now you need to help me decide. Which one?”

Sure Vinay. Let’s get a better understanding of each of the funds. That would automatically bring out the difference between the two.

Hopefully, you will get to decide the right one for yourself.

“That sounds good.”

You see, HDFC Prudence fund was started way back in 1994, as one of the earliest funds which had this proposition to invest in a mix of equity and debt, more of equity, less of debt. It is more rightly called a Hybrid Fund.

In comparison, HDFC Balanced was started only in year 2000 with a specified objective of having an equal mix of equity and debt. It planned to be truly balanced.

Over the years, HDFC Balanced evolved into a hybrid fund too.

One of the key reasons for this is to get tax benefits. As per current tax laws, funds that invest minimum 65% of their assets in equities are treated as equity funds and thus are tax free after 1 year.

“Oh! That is interesting to note. Tell me more.”

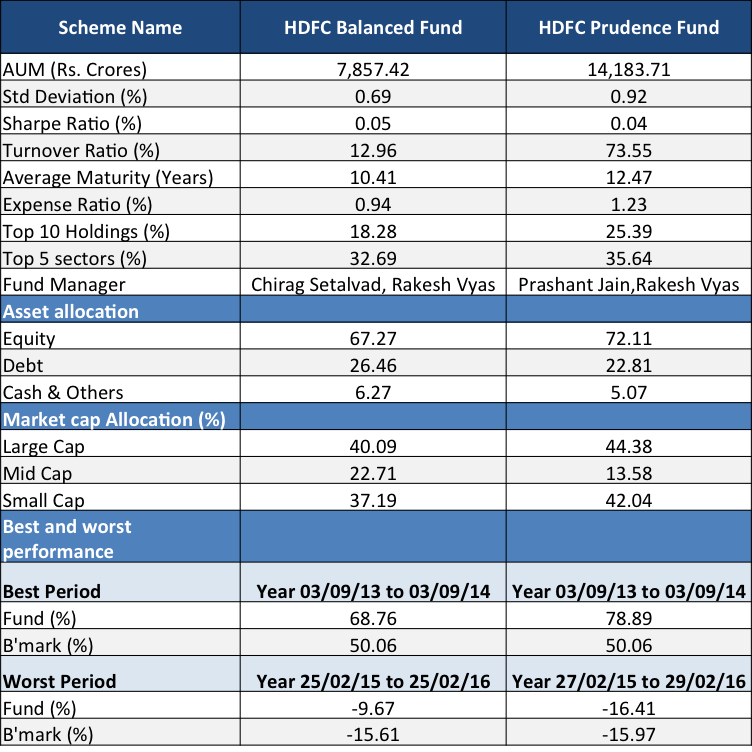

Have a look at this comparison table.

Data Source: Unovest

You can see some of the key parameters for the two funds. Only the direct plans have been considered. Direct plans of both the funds started on Jan 1, 2013. Numbers for Standard Deviation, Sharpe Ratio and Turnover are based on the last 1 year NAV data of the direct plans of the respective funds.

“What are the best and worst performance numbers here?”

Yes, that is a good pick. What they tell you is that for any 1 year period what was the best and the worst performance of the fund. Not a calendar year, but any 1 year in thee existence of the fund. In the same period, what was the performance of the benchmark.

You get to see the fund vs the benchmark performance in a new light. It is quite clear that HDFC Prudence had a better upside and a worse downside compared to HDFC Balanced.

HDFC Prudence operates in a higher range compared to HDFC Balanced. The Standard deviation number tells the same story. Note that the Standard Deviation for the past 1 year is at 0.67 for HDFC Balanced and 0.92 for HDFC Prudence.

HDFC Balanced still remains closer to 65% into equities and rest in debt while HDFC Prudence can invest as much as 75% in equities.

“So, can we say that HDFC Balanced is for a low risk taking investor while HDFC Prudence for a high risk taking investor?”

Well, since there is 65% + investment in equities, the risk profile is high for both the funds.

Also, HDFC prudence has a larger exposure to mid and small caps, more so the small caps, which are considered riskier.

The Average Maturity of the debt instruments is 10.47 years for HDFC Balanced vs 12.47 years for HDFC Prudence indicating that the latter has preference for longer maturity investments. Given the way debt funds are accounted for, this can lead to more than average volatility for the fund.

I guess what you are saying is that an investor who cannot take a lot of ups and downs in the value (in other words, volatility) is better off with the Balanced Fund.

“Yes, that’s what I meant. Frankly, I believe I am in that low volatility category.”

That’s fine. Even if you were not, I would put forth a question to you. Is the fund rewarding you with better returns for the extra risk you are taking? Measured by the Sharpe Ratio, you will observe that HDFC Balanced has a better risk adjusted return too. (see the table)

“But you know isn’t there a super fund manager at the helm of HDFC Prudence? Does that get it any extra points?”

You are giving too much weightage to a person. What if that person stops managing the fund tomorrow? Will you move out of the fund? It is better to stick to a fund that survives and performs irrespective of who is out there.

I would say that is actually a downside of the fund. Did you notice that having a super fund manager comes with its own costs? Look at the Expense Ratio.

The HDFC Balanced fund appears to run a tighter ship with just 0.94% of its value going to expenses. Simple, a lower fund expense ratio means more of the performance is available to the investors.

“Makes sense man. This was quite an eye-opener. I now know what to do.”

That’s good Vinay. Do look up the detailed factsheets of both the funds – HDFC Prudence and HDFC Balanced. (click on the links for the factsheets)

Between you and me: What else would you like to add to the discussion to help Vinay?

—

Disclaimer: This post is for information purpose only. The funds should not be considered as investment recommendation. Please consult your investment adviser before taking investment decisions.

Hello Vipin,

Nice article, with good reasons as always.

I need your help in identifying 2 funds for long term around 15 yrs, which is able to return around 15-16%. Little bit aggressive is fine and I am aware that there might be steep downsides in falling markets for such funds.

Thanks!

Dear Tridip

Thanks for the comment.

If you are looking for just fund names, can I request you to look up the MF portfolios service at Unovest? smart.unovest.co.

More details here: https://vipinkhandelwal.com/announcing-12-mutual-fund-portfolios/

Regards

what about HDFC CHILDREN FUND INVESTMENT PLAN ?

HDFC Children Gift Fund Investment Plan is more like HDFC Prudence, on the aggressive side.