This article assumes that you understand active vs passive funds. Click here to read the primer.

Index funds as well as ETFs or Exchange traded funds are very popular in US and Europe. So much so that Vanguard, the largest mutual fund company in the world, offers only ETFs.

ETFs follow a passive management style. They simply mimic the index in terms of its holdings and produce a similar return too. The cost of these funds is very less since there are no fund management charges or active trading involved.

Now, seeing the popularity of these funds, it comes as no surprise when the investor, more specifically, the NRI investor comes asking for ETFs and Index funds to invest in.

The reasoning is clear – beating an index consistently over a period of time is a difficult task. The investor is better off investing in an ETF based on an index thus save expenses and improve his returns.

Let’s test this hypothesis as of today.

Now, there are several market indices – large cap (Nifty 50, Sensex, Nifty Junior, Nifty 100, BSE 100), mid cap (BSE Mid cap, NSE Mid cap), small cap (BSE Small Cap, NSE Small Cap), broad market ones (BSE 500, Nifty 500), etc.

For the purpose of this post, we will focus only on the large cap ones, namely, the Sensex and Nifty 50. Both represent some of the largest, ivy league and bluechip companies.

Trivia: Just about 85 largest companies represent over 70% of the stock market capitalisation. We have over 5000 companies listed on the stock exchanges.

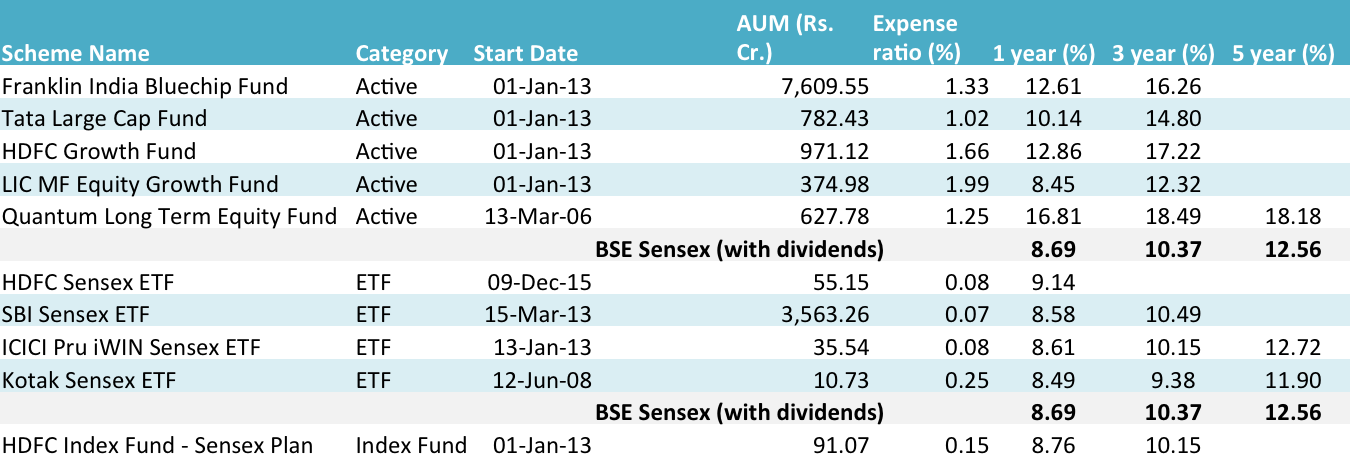

So, here is a comparison table of active funds, ETFs and index funds for each of the indices.

See the table below for Sensex based active funds, ETFs and index funds.

See the table below for Nifty 50 based active funds, ETFs and index funds.

Source: Unovest. All data is as on Jan 10, 2017.

For the purpose a fair comparison, I have used total returns of the index with fund returns.

Total Returns is the returns based on the change in price index plus any dividends. To account for the dividends, 1.5% (assumption) is added to the price index returns to arrive at the total returns.

The 1 year, 3 year and 5 year performance numbers are net of all expenses (pre tax).

Only the direct plans of active funds and index funds have been considered.

Observations:

- ETFs and Index Funds have underperformed their respective benchmarks (total returns), which is usually the case.

- The expense ratios of ETFs is in the range of 0.05% to 0.10%. The ETFs based on Nifty 50 have a lower expense ratio than those based on Sensex.

- Index Funds charge higher expenses compared to ETFs. They also underperform the ETFs roughly by the margin of additional expenses.

- Our indices are not considered very efficient in terms of construction. Yet not many fund managers have done a good job of outperforming them. For a fact, some of the actively managed large cap funds also invest in midcaps to bring in additional returns.

- A fund that stands out in under performance is HDFC large cap fund. It continues to charge top notch expense (2.1%) and the largest in the above selection and has delivered worse than the Index Funds or ETFs from the same organisation.

Should you invest in Index Funds and ETFs?

The primary purpose of an ETF or Index Fund is to take the fund manager and his cost out of the equation. A fund manager is required to generate alpha, to beat the index and bring additional returns to the investor by using research and insights.

As you would appreciate, most investors, retail or institutional, including mutual funds are largely focused on the large cap stocks. With so much scrutiny of each stock and every information related to it, it has become difficult to generate additional insights that can lead to alpha or extra returns.

This difficulty is going to only increase. It is likely that in the next 5 years active fund management in the large cap space will die. The passive index funds or ETFs would be a more attractive method to take exposure in that space.

For now, in the large cap space, it appears that active fund management has still a role to play. You need to ensure that you are picking the right fund and monitor it on a regular basis.

If you want to invest in passive funds then ETFs stand to be a better choice vis-a-vis index funds. (Please note you need a demat account to invest in an ETF and a demat account might incur you extra annual charges.)

Between you and me: So, what style works for you? Index Funds, ETFs or Actively Managed Funds? Do share your views in the comments.

Is there a list of the tracking error and expense ratios of all the index funds and Index ETF’s in India that is updated yearly on the net- this will make it very easy to decide which index fund or ETF one should invest in

I am not satisfied with the content but technically you are right so investors can take another option to invest their money.

This may be true in India. In the USA, it works the other way. For those who want to understand Index funds and ETFs should read Benjamin Graham’s “The Intelligent Investor”, Tony Robbins’s “Money-master the game” and a few others who talk about asset allocation and how in the long run you can’t beat the market, and neither can the fund managers. Of course, India is on a roll at the moment, but showing 3 to 5 years data is very limited. We should compare 20 to 30 years. I guess we have to wait for that to happen. Short term, fund managers are doing great. Its a matter of time (and I mean quite a few years from now), we may have to rethink our allocation strategy.

Rightly put Sridhar. It is just a matter of time. Thanks for the comment.

This is a strong recommendation for active funds. Looking at Nifty funds for a three-year duration, active funds generally beat index funds and ETFs.

Your conclusion that five years from now, active large-cap funds will die, is the exact opposite of what the data says so far 🙂 Let’s see how things turn out.

That’s right. We need to watch how things turn out.