For all the financial savviness that one might have, numbers still find a way to stump us.

This is what exactly happened with Vaibhav.

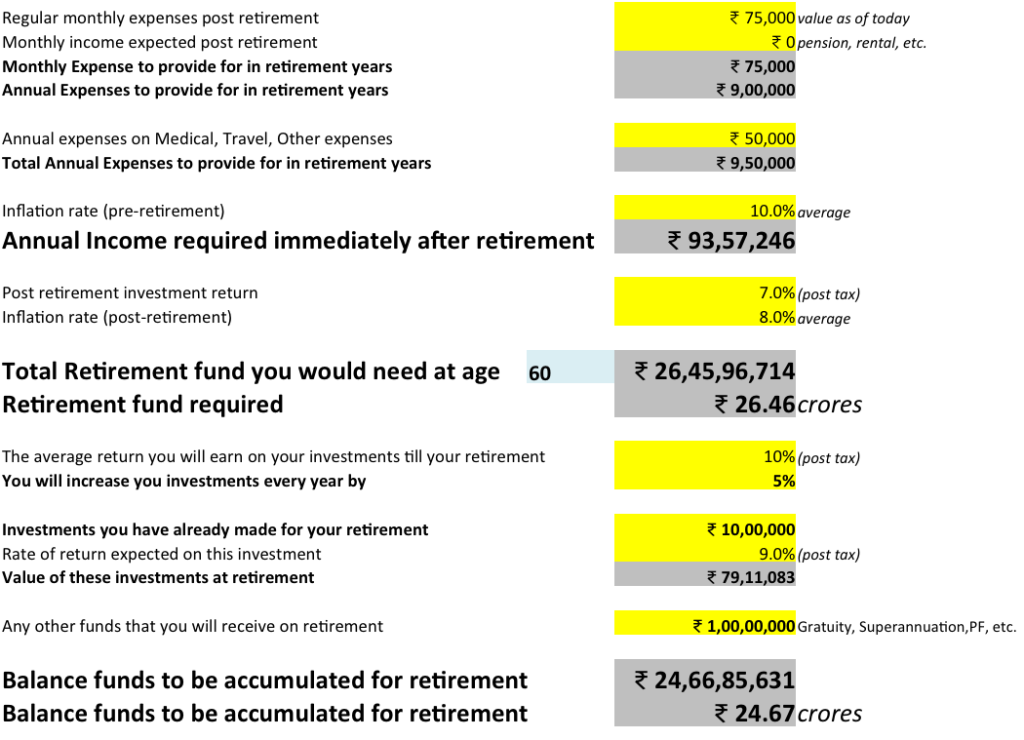

“You will need Rs. 25 crores as your retirement fund.” I announced to him after inputting the numbers in the retirement planning calculator. I was working with him on his financial plan.

“What! Really?” was his instant reaction.

“Yes. Why do you seem so surprised? Did you have something else in mind?”

“Well, I had done some back of the envelope numbers for my retirement. But this one is way off what I had got.”

“Hmm. What did you factor in as post retirement inflation and rate of return?”

“Well, I took more aggressive numbers – higher rate of return and lower inflation. Though I understand that it may not be the right thing to do. I also see that my life expectancy assumption at 80 is lower.”

“Yes, that’s a big mistake one can make. My question always is “what if you lived longer?”

“You are right. It’s better to plan for a longer life. Anyways, I guess I now know what I have to prepare for.”

So, this was Vaibhav – a 36-year-old corporate executive in a high-flying job, yet with a relatively simple lifestyle.

He wanted to plan for Rs. 75,000 monthly expense (not counting inflation) and another Rs. 50,000 per year thrown in for travel and health requirements. His life expectancy is 85. Since he is planning to retire at 60, he needs to plan for 25 years of post retirement.

When we did his Retirement Fund Calculation, this is what it looked like:

Apart from your regular expenses, you will also want to provide separately for some additional medical and travel expenses.

If you have been here before, you would notice this change along with a few others in the retirement planning calculator.

Now you can also account for on-retirement receipts like Gratuity, Superannuation, Insurance, etc.

The “how much you can increase your savings every year” was a recent change too.

And then finally comes the big number – how much do you actually need to save?

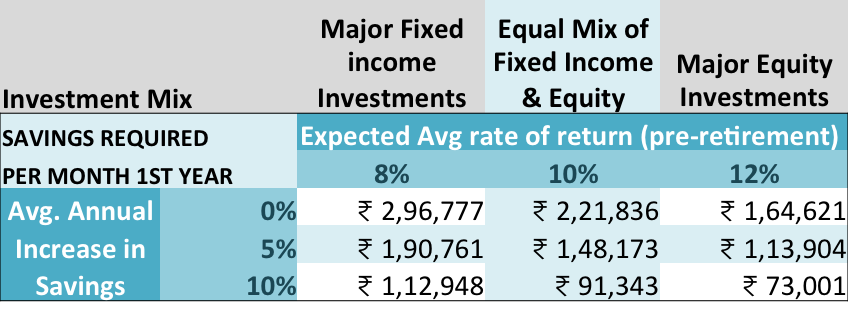

While the base calculator throws a number in line with your assumptions about inflation and return, you can now see an interesting perspective with 9 scenarios.

Saving for your Retirement – 9 Scenarios

We now know that Vaibhav needs to accumulate additional Rs. 25 crores approx. for his retirement. Given that he has 24 years to save and invest, the only other two variables that are required are Expected Return (pre-retirement) and Annual growth in savings, to find out how much does he need to save on an ongoing basis.

Now, the thing here is that he could choose to be conservative, moderate or aggressive with his investments and so he can expect to earn a return on his investments.

The second thing is that he can decide how much he can get his savings to go up every year so that they can work towards achievement of his goal.

These 2 variables thus influence his effort required.

I have made 3 assumptions for each of the 2 variables, thus giving a total of 9 (3*3) combinations.

See the matrix below.

You can pick one of the return numbers based on whether you are fully interested in equities, somewhat interested or not at all interested in investing in equities.

And then you pick from whether you plan to increase your savings every year and how much. For simplicity sake, Zero, 5% and 10% have been taken as assumptions for annual increase in savings.

If you are choosing an annual increase in savings scenario, then you need to keep in mind that every year you need to increase you savings by the rate you have chosen.

So, if Vaibhav is a moderate investor and he would invest in an equal mix of fixed income and equity. He also feels that he can increase his savings by 5% every year. With these 2 variables defined, he needs to save Rs. 1.48 lacs every month for the 1st year. This monthly saving needs to go up by 5% every year.

Do your own retirement planning

Download this Updated Comprehensive Retirement Planning Calculator Excel Workbook

When you open the excel workbook, you will see 2 sheets. One is the retirement calculator and other shows you the 9 scenarios.

To view the scenarios, you should first use the calculator to input your numbers in the yellow cells only. Let the numbers then tell you the story.

Use the scenarios to understand what would best suit your investing style.

Trust me, this exercise is far more important than buying that endowment, money back, pension plan or a mutual fund.

My question to you now is – Does retirement look closer? What change do you need to make, if at all, to make your retirement funding plan work better for you?

What are the questions you are asking? I would like to know them in the comments.

Hi Vipin,

One suggestion, can you please add corruption index to this calculation? It is rising faster than inflation, so in 20 years time this will be an even bigger factor than inflation.

For eg, in 15 years from now, we may need to pay bribe for redeeming mutual funds, withdrawing money from bank, buying food items, traveling in a bus, etc.

Dear Pradeep,

My apologies if this has hurt you in any way.

What makes you feel so pessimistic?

Hi Vipin,

I am not very pessimistic, but just reiterating Corruption is a fact of life. Let me give you my experience.

I wanted to construct a home on my plot for which I submitted a plan for approval in a govt office. The officer dragged it for 4 months and still to give approval, he demanded 10k as bribe which is to be divided between him, local councilors and his office mates. So that is black money in the hands of 10-15 people. Imagine he will approve 30 such plans a month and they will earn anywhere between 4-5 Lacs a month as bribe.

Now why does he demand a bribe? Any govt employee gets his job by paying a bribe. He gets promotions by paying bribes. This along with pressure from politicians make him demand bribes.

Do you think this vicious cycle will stop in the near future? Answer is No.

Okay what has this got to do with our retirement life?

Let me explain that.

These bribe takers and real estate agents grow the black money culture. They hugely outnumber the tax payers. Only 3% of the Indians pay tax. Lets say 50% are poor and the remaining 47% don’t pay any tax and have lots of black money.

Now check out how much a school charges for admissions, its 30k and upwards along with 100k donation for kindergarten. It has risen 10 times in the past 20 years which puts the inflation close to 50%.

Why would this happen? When you have 47% of people with lots of black money, they are ready to pay anything for education, medical, etc. This in turn increases inflation for all these things. 7 or 8% inflation does not apply to any of these.

Now where does all the theoretical retirement calculation stand here?

In 20 years time, in the name of helping poor, govt will start taxing more on our savings. A Mutual Fund redemption can be charged, bank withdrawals can be charged. Afterall the poor people voites count more than the 3% of tax payers and MF savers. Govt will not try to stop corruption as it is the bread and butter for their cadres.

You may go to court, but the pending cases will only increase from the current 3 crores. When will you get justice?

We can be optimistic in life but cannot be ignorant of the facts.

To give you an analogy in financial planning, we are optimistic by saving money for retirement, but not ignorant of any unforeseen events by insuring ourselves.

You are welcome to disagree with my views.

I cannot disagree with what you have gone through. I have had my own such experiences in the past. However, I only see things improving.

A simple example, I am sure you have heard horror stories about IT deptt. This year my IT return got processed within 1 week of submission and the refund amount was credited the next day to my account. In the past refunds have taken years to come and probably that too when you kept knocking at the doors.

Of course, we can see some improvements in several things around us, like you mentioned Income Tax Refund is one of them. But we have to remember that this is only getting a refund, if any was paid in excess as tax.

I guess a lot of us have made huge improvements in tax planning as a result of which our refunds are very minimal these days.

They are making taxpayers pay their tax properly, not a bad thing. But when will they make tax evaders pay tax?

When will they punish corrupt citizens who are drinking peoples’ blood?

Unless they do that, the black money fueled inflation will punch a big hole on our retirement and other calculations.

Even Equity can give only 15% long term returns which is no match to the real inflation that matters which really is 40-50%.

Thats where I suggested Corruption Index in our calculations.