“I want to retire at 50” Dinesh announced, “and then just enjoy life – reading, cooking, writing, everything that I always wanted to do.”

“That sounds like a plan Dinesh. But are you ready to do it?”

“Means?”

“I mean, are you financially ready to retire at 50?”

“I guess so. I am saving up enough that I can live carefree till 70.”

“How do you know you will live only till 70?” I paused. “What if you lived longer?”

“Well, no one in my family has lived beyond that age”, he winked at me. “Plus, isn’t that the normal life expectancy of a urban male in India”, he turned the screen of his smartphone towards me. The Census of India site confirmed the life expectancy number. I took his phone and read further.

“Do you notice here that the life expectancy has been continuously increasing over the years? There is a fair chance that you could go on to live till 80, 90 or even 100.”

“I don’t want to live that long.”

“I am not saying you have to. I am saying you may. In that case, will you have enough money to take care of you and your wife?”

This got Dinesh thinking. After a couple of minutes, he replied, “I don’t know.”

He looked at me and said, “You tell me. What would it take?”

What if you lived longer?

I had just been working on retirement planning for various life expectancy numbers. I opened my laptop and turned the screen towards him.

“Here, see this.”

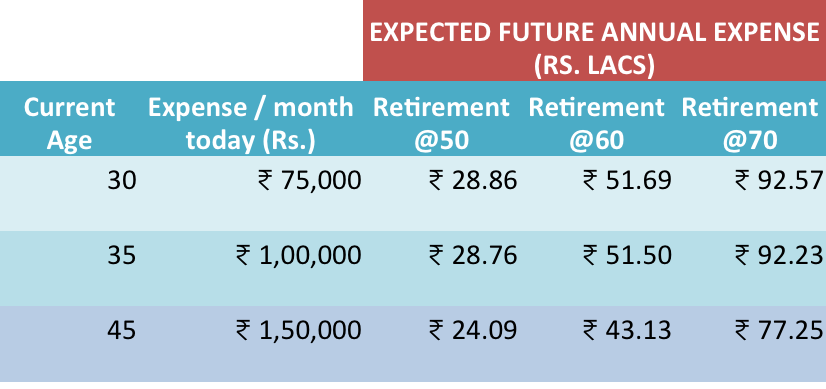

“The first thing that you need to know is what will be the future value of your expenses. In this table, you can see the future expenses values for 3 different ages – 30, 35 and 45, and 3 different retirement ages – 50, 60 and 70.

Dinesh, you are 35 and I think that your monthly living expenses are close to Rs. 1 lac per month. Correct?”

“Yes, that’s right. Give or take some.” Dinesh confirmed.

“So, you see that if you want to retire at 50, just a 6% inflation per year will ensure that you have to cough up approx Rs. 2.4 lacs a month or 28.76 lacs in one year.”

“Well, I realise that expenses would go up. But that’s not the number I had thought. It’s huge. But I am thinking that my decision to retire early is right. Because the more I delay, the higher the expense requirement will be. If I retire at 60, the expenses are almost half a crore a year. That is like Oh my God! ”

“That may not be the right way to look at it. Just hold on to that thought for now. Let’s now see the more important part. Here.”

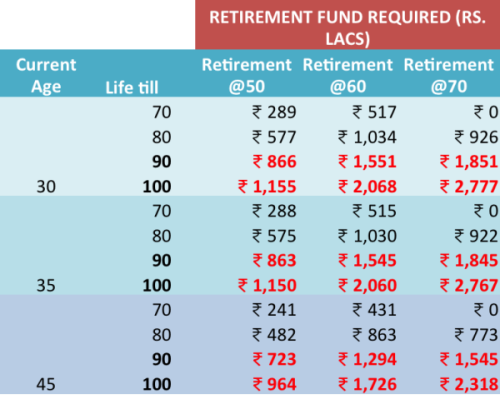

What if you lived longer – retirement fund required

“This table shows that if you were to live for 70, 80, 90 or 100, what is the total retirement fund you would need to not worry about money at all later? You need to see this carefully.”

“If you were to live till 80, you would need almost Rs. 5.8 crores at age 50, to live your entire post retirement period. If you were to live till 90 or 100, the number goes up significantly to Rs. 8.6 crores and Rs. 11.5 crores respectively.”

“But honestly, I don’t want to live so long.” I could see Dinesh’s disbelief.

“Don’t be stupid. You have so much to contribute to the world with your talent.” I almost scolded him.

“How will I ever save so much? I can’t compromise on how I live today.” Dinesh was defensive.

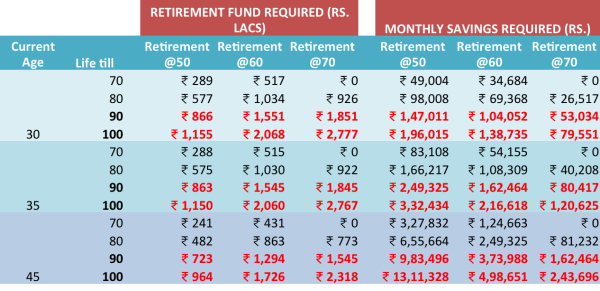

“OK. Let’s look at that now. How much do you need to save?”

I scrolled the excel sheet further to come to this point.

“Here is the amount you need to save monthly to reach your target goal of retiring at 50. Let me throw in some assumptions here.

The first one is that you have not saved at all so far. The second is that your savings per month will be constant number for the next 15, 25 or 30 years. The third is that till the time you retire, you will get a rate of return of 8% post-tax on your investment portfolio.”

“What nonsense is this? Rs. 3.3 lac savings a month? I would never be able to do this.” Dinesh’s eyeballs rolled as he looked at the numbers. “You see all the more reason to not live longer. I hope they allow euthanasia by then. Else, I will go to the jungle and take samaadhi.”

I couldn’t stop laughing.

“Don’t worry my friend. There is a smart assumption we need to make and life will appear much better.”

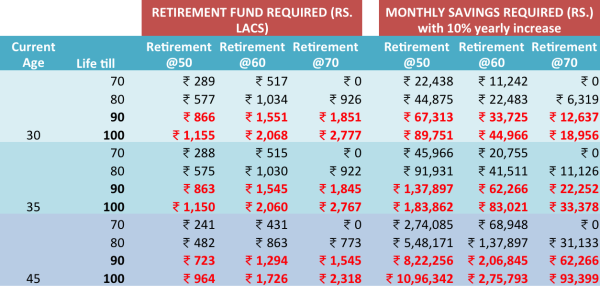

“See this”, I scrolled the screen further.

Dinesh was surprised and instantly shot a barrage of questions. “What did you do? How come the numbers dropped so much? Is your formula working right?”

“Hold on my friend.” I said as I kept a hand on his shoulder. “As I said, we made one smart assumption here. We will now increase the savings by 10% every year. What it means is that you will start saving Rs. 22,252 per month this year and then next year take it up to Rs. 24,477 per month. Every year, you will save 10% more than the previous year. All that put in the right investment portfolio will still give you the retirement fund you are looking for.”

Dinesh looked at the table with deep concentration. “Aha! That’s a good one. That is how it will work out in reality too.”

After a pause, he said, “OK. I see your point. I think I should plan for a life expectancy of 90 years. Honestly, it gives me goose bumps thinking that I would have to live for so long and worse, depend financially on anyone at that age. Better prepare myself to be on my own.”

“You are absolutely right Dinesh. I understand the numbers might look a little hard for now but they are definitely achievable. You just have to ensure discipline and patience with your savings and investments.”

“You are right. I now understand the enormity of the goals. I need to be more careful of where and how I invest. All these years, I haven’t paid much attention to money.”

“Anyways, thanks so much for this revelation. I guess I have some homework to do. I am going to come back to you to plan this out for me and help me invest and monitor too.”

“I am glad Dinesh, I can be of help. There is one more point you can think about. Instead of planning to retire at 50, you can plan out your life to retire later. This can be done in a way that gives you lot of time to pursue your interests. Why wait for a later age to live the way you want? Do it now.”

“Yes, that is a good point too. And the financial requirements too go down a lot if I work longer. Good. I will think about it too.”

“Let me know when you are ready.”

“Yes of course. Need to give it my best shot. Otherwise jungle to hai hi. (I can still go to the jungle)“. We both laughed.

Between you and me: What if you lived longer? Do share your suggestions and feedback in the comments section.

Could you please explain how the retirement fund required at 60 could be higher than the fund required at 50?

If I work for 10 more years (50-60), I would need lesser money in my retirement fund, right?

What am I missing here?

Good observation. It does seem like a paradox, courtesy inflation. What you really need to look at is the money required to be saved to have this fund. Thanks for reading and the comment.

Very Nice Article, I also try to convince ppl around me about this.

Thanks Rohit. You are doing a good job. 🙂

Good one vipin.

In one way, it is nice and good to plan for as much longer as possible.

But considering the income limitation, its difficult to put everything for retirement at the expense of other goal.

So i think along with the retirement planning, one should also look to being an elderpreneur seriously.

Just to add, along with income limitaiton, there are various other factors like inflation, interest rates, return from equities on which your retirement corpus is dependant on. So instead of just depending on the factor which is not in our control, its better to improve ones skill (which is in our control)and become an elderpreneur.

I second that thought Dinesh. Thanks for the comment.

Hi Vipin,

In India, Rich are thoroughly CORRUPT & In-line with Politicians/Bureaucrats – So, they need financial planning to hide the Loot.

Middle Class is always struggling to make Two -ends meet, pay taxes,save for Retirement,Medical etc., in the absence of ‘Social Security in India( Dies one day struggling).

Poor People in India, NOT affected by Inflation,Taxes, etc.,Have Zero Hope from CORRUPT Govt Machinery and live for a day, since last 70 Years of Independent India.

Unless, one leaves India behind and settles in US/England etc.

I have been saving from my meager Income regularly for the last 40 years; Firs, in Bank Deposits, then in Shares & Stocks, then in Mutual Funds etc. and still could NOT create a corpus of 1 Cr, till date…. All so-called Financial Advisers have been sending me Bills for early payment with ZERO responsibility for Better returns (To beat Inflation & Cost of Living) …. So, even today we (Middle Class) are struggling to live in our beloved India …. Bharat Mata Ki Jai Ho !!!

Dear Shri Pandher,

I am an eternal optimist.

Be patient and keep yourself on the track is all that I can say.

Thank you