In my recent workshop in Gurgaon, one of the topics that came up for discussion was “child’s education”.

One of the participants, let’s call him Ashok, mentioned that he pays Rs. 25,000 a month as fee of the school where her daughter studies.

It ensued a debate on how education expenses have risen dramatically over the past 10 to 15 years.

Ashok himself incurred only about Rs. 1 lac to complete his engineering – 20 years ago though.

Yet another participant mentioned that he spent just about Rs. 2 lacs as fee for his engineering and MBA.

I couldn’t resist mentioning that my own MBA – all tuition, lodging, travel and fun expenses included was completed in less than Rs. 1.5 lacs.

In fact, my entire year school expenses including fee in Class 10 was Rs. 10,000 only. This is a far cry from the fee of Rs.25,000 a month that Ashok pays for his daughter.

Of course in all these cases, the people went to Government funded and subsidised institutions, which charged only a nominal fee.

Times have changed though. The government institution doesn’t cut it any more.

As a parent, the one thing that you want to prepare your child for is to be ready for life in the best way possible. You want to equip her with the necessary skills and knowledge. You want the child to have an exposure that enables her do her best in life. You want her to stand on her own feet.

There’s a new breed of educational institutions (Schools, Colleges, Universities) that promise the fulfilment of these conditions.

You want the best for your child. Period.

However, what does it mean to you in terms of money? How much would you need to invest for your child’s education?

Education is damn expensive

One thing is given that the new education does not come cheap.

Ashok pays more for his child’s school fees than the rent of the house he lives in.

The child is still at Primary School. Then there will be High School, College and the University.

Hopefully, with the firm foundation that the child will create for herself in the early stages, the need to fund her higher education should not be very high. The child can also avail of several scholarships available these days.

But as you would agree, the scholarship may not come through or even if it does, it may not be enough. You would not want to let yourself be unprepared in case a full funding is required.

So, that brings us to the question. Will you be ready to fund your child’s education? Are you saving enough?

You can find the answers with this new Savings for Child Education – Calculator. But before we get there, let’s understand the cost for Ashok’s daughter’s education and the savings required for it.

The real cost of education and saving for it

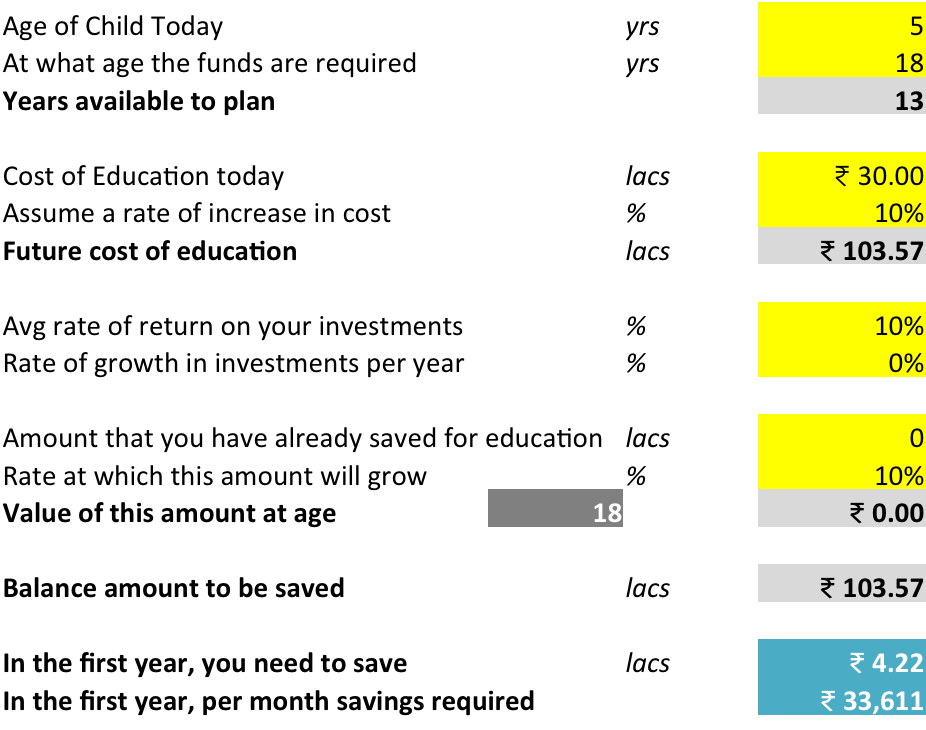

In Ashok’s view, if his daughter, Rhea, plans to do engineering, it will cost Rs. 30 lacs at least. This is today’s value, not counting inflation.

Rhea is 5 today and she will start her engineering at 18, that is, 13 years from now.

Assuming that education costs rise at 10% a year on an average, Rhea will need over Rs. 1 crore (Rs. 1.03 crores to be precise) for her engineering education.

Yes, that Rs. 30 lacs of today for an engineering course will turn into Rs. 1.03 crores in 13 years.

Now, to achieve that figure, Ashok needs to save Rs. 33,610 a month for the next 13 years. This assumes that he averages a 10% return on his investment during this period.

If he were to earn 8% per year return on an average, he needs to save Rs. 38,700 a month, that is, Rs. 5,000 extra per month.

Does that make your eyes open wide?

Now, I know these numbers may not apply to your needs.

So, I have done something for you. I have made this simple calculator which you can download and use it with your own assumptions. Nifty, isn’t it!

Click to download the Saving for Child’s Education Calculator

The fields are pretty straightforward. Just ensure that you input only in the yellow coloured cells.

I know what you are thinking now.

How do you earn an average return of 10%? Where should you invest?

In a previous post on retirement fund planning, I had suggested the following:

- To earn an average return of 8%, you will have your investments predominantly in fixed income / debt based investments. These include Bank FDs, EPF, PPF, NSCs and some tax saving mutual funds.

- To earn an average return of 10%, you will have to move further towards equity – say a 50:50 ratio between fixed income and equity investments.

So, your choice of your investments should take into account this factor.

Please note that these assumptions can change significantly over time.

Beware

All said and done, your child’s education is an emotive issue for you. And that is what some products use to manipulate and sell you investments that are not the right fit for your needs.

As an example, Child Education Plans offered by Insurance Companies are not the best investments. Don’t lock in your money in an inflexible, high expense and low return investment.

Ashok made the same mistake too investing in a Smart Kid policy.

A smart kid policy may not end up making your kid smart.

Nor do the endowments and money backs in whatever fancy avatars they may be sold to you.

A mutual fund sold in the name of Children’s career may not be the right investment too. These mutual funds are more like debt products. They are not tax efficient as well.

But see what your calculator tells you. After that, you have two choices – either save more over time or make your investments perform more.

Ashok has realised this and now is restructuring his investments to ensure that his daughter Rhea gets the education she deserves and becomes a responsible and contributing citizen of the country.

How are you planning for your Child’s education?

Hi Vipin,

Likes the info you have shared. Kindly advise how can i save for my new born baby for education and marriage.

I have no knowledge about equities, shares. So what arenthe investment options?

Hi Vikrant

Congratulations for the new born!

I think before you jump into it, spend some time learning about it.

Here are a couple of articles you might want to go through:

10 money basics that you must never forget

The no secret couple to get your networth soaring

Your Ultimate Money & Investing Checklist

Equity Investing – As I understand it!

Equity Investing – Let’s get this straight!

Are you aware of these 20 mutual fund facts?

Treat your investments too like your children. Start learning.

Happy to hear your questions.

Cheers

It is very nice post Mr. vipin, but the fees(25,000) you said for child education is too more compare to normal fees of education. I do agree with Mr. Pradeep, I think they don’t need such costly school training to sustain their brilliance. Plain straightforward schools are better than average school instruction with a touch of consideration at home will bring them up so pleasantly.

Thanks for reading and the comment Deep. As I mentioned in the other comment too, to each one his own. We all make our choices.

Vipin,

25,000 per month school fees for a 5 year old child? Are you serious?

Did you inquire Ashok if they are teaching medicine to her daughter already?

I have seen very smart kids who have not started school yet and I believe they don’t need such expensive school education to nurture their smartness. Plain simple decent school education with a bit of care at home will bring them up so nicely. And those decent schools will charge no more than 40k to 50k per year including books and travel in a metro.

This is similar to many fin planners prescription of plain vanilla mutual funds for investment instead of fancy schemes.

The fact that there are people ready to pay 4-5 lacs for kindergarten is making our education inflation grow nearly 50% every year.

At this rate how much ever you save, if won’t be enough.

Dear Pradeep, I had exactly the same expression with me as yours when I heard the number. I would also agree that there are fairly decent schools out there which charge fees as mentioned by you. But to each one his own.

hi vipin

very usefull infomrmation keep it up.

Thanks Raja.