No one wants to buy index funds

The concept of Index funds has not worked in India, at least not so far. They are super hit in countries like the USA but not in India. Vanguard in the USA, the largest mutual fund company, has all its products as index funds.

Further read: Founder of Vanguard, John Bogle’s 8 Rules to build your mutual fund portfolio

Less than 1% of the overall investments in equity mutual funds in India are in index funds. That says it all.

The one word that would come to anybody’s mind who is picking mutual funds is ‘performance‘, which again, for index funds, is nothing to write home about.

There are several ‘other funds‘ that have delivered much better returns. And is that not what we want – more returns?

The ‘other funds‘ are the ‘actively managed‘ funds compared to the ‘passively managed‘ index funds.

Having said that, there are some key benefits of using index funds as a part of a long-term portfolio. Let’s explore them here.

Quick Primer on Active and Passive Styles of fund management

(Skip this section, if you are already aware about the styles)

If you are new to the jargon, an actively managed fund is the one where the fund manager takes call on what should enter the portfolio, how much and when. The fund managers call the shots based on several parameters that they have outlined as a part of the investing process.

In contrast, a passively managed fund does not need a fund manager. Not literally. Someone does need to take care of the investor’s money. The difference lies in the fact that an index fund simply invests its money in a pre-identified portfolio of stocks. This pre-identified portfolio is usually a popular market index.

I am sure you have heard of Sensex, Nifty, etc. They are popular stock market indices. Sensex for example is a bundle of 30 large stocks that are listed on the Bombay Stock Exchange (BSE). Nifty is a collection of 50 such stocks that are listed on the National Stock Exchange (NSE).

The 30 of the Sensex or the 50 of the Nifty also have predetermined allocations for each of the stocks. These allocations change over time as markets grow, companies grow – that’s a different story though.

An index fund has a simple job. Just take a look at what are the stocks and their respective proportion in the market index is. Invest the money in exactly the same stocks and in exactly the same proportion.

After that it has to ensure that the stocks and the proportion remain in tandem with the index. If the proportions change – the fund manager shuffles the portfolio to reflect the new ones. That’s it.

Unlike active fund management, there is no research involved and no extra effort in figuring out which stocks to buy, at what price and when.

Suppose I launch Unovest Index fund – Sensex Plan. I have to simply look at the 30 stocks of the BSE Sensex and invest my money in them in the allocation that is already in the index. Wow! I got a ready-made portfolio.

I hope you get the reason it is called passive.

The success of the index fund is measured in how close it is able to replicate the performance of the underlying index it is copying. Yeah, and there is a term for that – tracking error. The lower the tracking error, the better the fund is.

On the other hand, the active fund‘s job is a tough one. It has to beat the underlying benchmark returns. After all that is what you expect, right? Take for example, Franklin India Bluechip Fund. The fund benchmarks itself against the BSE Sensex. The fund will work to deliver a performance better than the BSE Sensex. Hence, it will carry out necessary research and analysis, create investment strategies and decide which stocks and companies make the best investment opportunities.

Isn’t that a reason you will invest in an active fund like that? Else, you are just better off investing in an index fund.

Hopefully, you have understood active vs. passive fund management. Now, let’s have a look at the performance bit.

What about performance?

In the tables below, I have taken some well-known funds from 6 mutual fund companies. There is at least one actively managed fund and one passively managed index fund from each one of them.

To differentiate, the index funds are in blue colour font. Against every fund, its benchmark and the performance of the benchmark are also shown. The benchmark is in orange colour font.

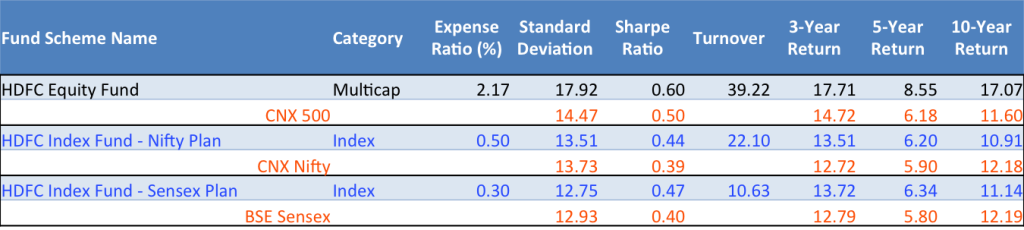

HDFC Mutual Fund

One of the most popular schemes of HDFC Mutual Fund is the HDFC Equity Fund. In recent times, its performance has taken a setback. However, at one time, it used to be a fund to swear on. Within HDFC, I have picked their Index Fund – both Sensex and Nifty Plan.

It’s interesting to note that the Index Funds also have beaten their benchmarks. This is because the index does not take into account any dividends, bonus, etc. that an index fund receives by the virtue of its actual holdings.

Also read: The HDFC Large Cap Fund which fails to beat the index

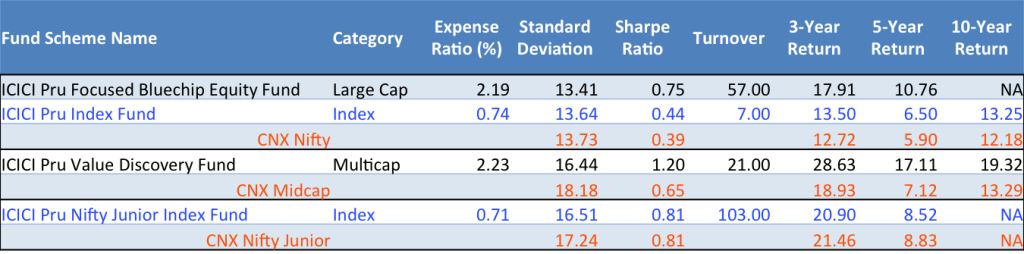

ICICI Pru Mutual Fund

ICICI Pru has two schemes, which are hugely popular these days – Focused Bluechip and Value Discovery. The former is a large cap scheme and benchmarks itself to the Nifty. The latter is more of a mid-cap fund and benchmarks itself to CNX Mid-cap.

The two index funds from the house I have taken are the ICICI Pru Index Fund and Nifty Junior Index Fund.

Franklin Templeton Mutual Fund

The flagship scheme from the Franklin Templeton House is the Bluechip Fund, a true blue large cap fund. The passive counterpart of Bluechip is the Index Fund – NSE Nifty Plan.

UTI Mutual Fund

In case of UTI, we have taken UTI Opportunities Fund and UTI Nifty Index Fund.

Reliance Mutual Fund

Reliance’s Focused large cap fund and the Index Fund help you assess the performance from the perspective of two indices.

Birla Sun Life Mutual Fund

Finally from Birla Sun Life, the Frontline Equity Fund, benchmarked to S&P BSE 200 and the Index Fund with Nifty as the benchmark has been taken up.

Note: All data has been sourced from ValueResearch and is as on Oct 9, 2015.

Overall, a few more observations are in order:

- There are a variety of benchmarks that the funds use. From the popular ones like BSE Sensex and NSE Nifty to CNX 500 (HDFC Equity), S&P BSE 200 (Birla SL Frontline Equity), CNX Midcap and S&P BSE 100. Though Nifty seems to a favourite among the funds.

- As you can see, in terms of returns, active funds have, in every single case above, beaten their respective benchmarks – that too by quite a margin.

- On returns basis again, the actively managed funds have also beaten the index funds from the same fund house. Quite clearly, the active strategy has won hands down. [Read more: Using Index Funds instead of Total Return Index for comparison]

- All index funds or passively managed funds have a very low expense ratio compared to their actively managed counterparts. It ranges from 0.3% to 1.05%. The low expense ratio is a result of savings on costs of research, analysis and frequent trading of stocks.

- The turnover ratio of the index funds too is much lower than the active funds, except in some cases. The need to change stocks frequently is just not there and that explains a lower turnover.

Whatever one may say, when you select funds, it’s the performance that you count on. You want the most bang for your buck, literally.

Given that, who wants to buy into boring, underperforming index funds then?

Not really.

Why Index Funds?

Yes, index funds just do not make the cut on performance. But, that is not the only reason for which they should be ignored. There are benefits of investing in Index Funds too.

Here are a few reasons you might want an index fund in your portfolio.

#1 You do not believe in fund managers

Fund managers are humans, after all. They can pick bad stocks, they can mistime the market, they can ignore long term trends and they can be a victim to various biases. You are not comfortable subjecting your money to a fund manager’s whims. Index funds are for you, totally.

#2 You want to play a low cost strategy

The only thing that you can truly control is your costs – be it in business or in investing. By eliminating the research costs and lower turnover costs, you play an absolutely low cost investing strategy. All these low costs ultimately add up to your returns.

#3 You want to be fully invested in equity, at all times

As a smart investor, you decide your own asset allocation, that is, how much money should be invested into equity, bonds, real estate, gold and cash. For your equity portion, you choose equity mutual funds. You expect your mutual funds to be 100% invested in stocks all the time – in alignment with your asset allocation.

Now, if the active fund manager decides to hold cash based on his analysis of the market, it distorts your asset allocation. You hold cash PLUS your fund manager also holds cash = Lots of Cash in your portfolio. It could also mean missing out on investment opportunities.

The way out could be a passively managed Index Fund. Most index funds are, usually, fully invested in the index stocks, since their mandate is to mirror the returns of the underlying index. Yes, the returns may not be close to actively managed funds but then you are more concerned about your asset allocation.

Pro Tips for Buying Index Funds

So, now if the idea of index funds is appealing to you, here are a few pro tips to get you going.

Pro Tip 1: If you plan to have an index fund in your portfolio, it would be best to have a broad based index fund. What I mean by that is an index that captures a large part of the market, such as a CNX 500. The Goldman Sachs CNX 500 is one such fund. Please note that this fund is not a recommendation but only an example.

Pro Tip 2: If you are a beginner in stock investing, an index fund could be a good idea to start with. It gives you exposure to a large broad-based portfolio at a very low cost.

Pro Tip 3: You can buy index funds directly with a mutual fund. However, some of these funds are also available as Exchange Traded Funds or ETFs. This makes it easy for them to be bought and sold just like a stock. You can use your demat + trading account to buy / sell one anytime.

So, as you can see Index Funds can find a place in a portfolio, of course, with certain considerations.

Further update: Are ETFs and Index Funds better?

Between you and me: Are Index funds for you? Looking forward to your comments.

Hi,

I’m an NRI and have the option of investing in the Indian and/or the US markets.

Do you recommend index funds in the US markets?

Thanks

hi, I Am not qualified to talk about investment products in US market.

Hi Vipin

Amazing article…exqctly what I was looking for. Would be great if you can advice on the following too:

(1) I want to invest lumpsum and not loose my principle……need money in next 5 years. Which bond fund should I nvest in ( dynamic, short term, liquid etc). Also if you can name some good funds

(2) Looking to invest in USA index fund. My understanding is only one ETF with good performance is there…. MOST nasdaq 100 etf…..any other you are aware of? Particulary looking at S&P 500…….I am not cmfrtble investing directly through intl brokers as involes random taxes plus risk of policy changes.

Hi Rohit

Thanks for the comment.

1) Please read this: http://www.unovest.co/2016/06/ultra-short-term-funds-alternative-bank-fd/

2) Don’t see options for US ETFs. Here’s the factsheet for MOST Nasdaq 100 ETF – https://smart.unovest.co/pages/scheme-details.aspx?schemecode=CL0/A2ANYos=

Hope this helps.

Hello sir

I’m a complete beginner to the stock market. Motivated by “rich dad,poor dad” and “the rules of common sense investing”, I wanted to invest in the stock market as I turn 20 next week.

Also all the popular material out there is in accordance to the markets of USA. And as I read in one comment, cost of mutual funds are comparatively lower in India.

Could you please suggest some books for the Indian stock market.

Thank you!

Dear Madhurima

I am not sure if there are any specific books for Indian Stock Market. Thankfully the Internet presents you with an opportunity to access brilliant minds and their thinking about investing.

I would recommend that you search and read various such blogs/websites and then subscribe to those that you feel help you.

Thank you

Have Balanced funds returned better than index funds over the longer term? Which would give better returns and capital appreciation, given an investment horizon of at least 5 to 10 years?

Dear Percy

You will have to first appreciate the fact that index funds do not need any fund manager inputs. it just mimics the index in question. Also, assuming it is an equity index fund, it will be 100% invested in equity only. It is fully exposed to the vagaries of the market and the underlying index.

As far as balanced funds / hybrid funds are concerned, the money is divided in some proportion between equity and debt and both the components are managed actively by a fund management team. The presence of debt itself reduces the risk profile of the fund and the constant reallocation ensures that the returns profile also remains consistent.

With that perspective, let me share that balanced funds have delivered more performance than index funds – as far as India is concerned.

Sir can you please suggest good books on the Indian stock market,investing,day trading,etc for a total beginner. Thank you in advance.

Harshitha,

If you are a total beginner, you should focus on understanding and strengthening the fundamentals of not just investing but a whole lot on how to improve your thinking process.

So, while you read “An Intelligent Investor“, you would also want to read “Fooled by Randomness“.

“Poor Charlie’s Almanack” is also highly recommended.

There are some really amazing blogs out there too. http://www.farnamstreet.com, Prof Sanjay Bakshi’s blog, etc are a couple of them.

Stories of Panchatantra shouldn’t be missed either.

Hope this helps.

Tony Robbins says in his book Money:Master the game, that we shouldn’t invest in mutual funds as there are many hidden charges. What do you have to say about that Sir?

Tony Robbins speaks about the US market. In India, mutual funds are one of the most transparent and low cost investments. We don’t have upfront sales loads. In US, this cost itself can go upto 7%.

Thank you for the information.

I wanted to know about the total number of index funds launched in india, from where can i get this information?

Monika, you can get this information from AMFI or SEBI, I think so.

You can also look at one of the online mutual fund information portals and use category selections to know all the funds that are there currently.

Hope this helps.

I think you picked the well known top performing funds and bench-marked them against the underlying index funds. Roughly 30% of total active funds outperform index over a 10 year period. Only 15% of actively managed funds will outperform index funds over 20 year period. So which active funds should I put my money on is the important question and is not easy to answer. Assuming that funds which will beat index over 20 years will come from the ones which out-performed index for first 10 years, my chances of picking a fund which will beat index for 20 years is 50%. Hence the importance of investing in index funds in India.

Not true. I identified the top 10 actively managed funds and index from a decade back (that is, funds that had the best performance from 1995 to 2005). The median actively managed fund in this list had a 10.something % annualised return, while the index fund had 8.something. If you’re interested, give me your email ID, and I’ll mail you the spreadsheet

Hello Kartick,

Could you send me the spreadsheet you mention in your response? My email is ssockalingam@gmail.com. Thank you.

Regards

Sridhar

Thanks for the comment Ashish. I agree with your point of “so which active funds should I put my money on is the important question and is not easy to answer.”

Having said that, index investing still has some time before it can work in India. The margin by which these funds outperform the benchmarks is huge. Even if the funds languish in comparison to the category, they have outperformed the benchmark. This probably suggests that the bar (the benchmark) is not good enough.

Typically, the broad market indices are used as benchmarks so that debate need not arise. How those benchmark indices are structured is something that needs to look at.

We should speak again in 5 years and see how index funds are doing. They would become relevant one day, for sure.

Hi Vipin,

Although mutual funds perform better than index funds over the long run, adding tax on realized gains to the costs, mutual funds do not look superior to index funds. What do you think?

In India, if you hold the equity funds for more than 1 year, the gains are tax free.

Hi. Vipin, can u suggest me an index fund with a broad Indian market exposure and lowest expense ratio.. Just like Wiltshire 5000 index or S&P 500 in USA…?BTW thanks for ur input.

Dear Hameed, Thanks for the comment and the ask.

The only fund I see based on the Nifty 500 is GoldMan Sachs CNX 500.

Have a look at the details here. https://smart.unovest.co/pages/scheme-details.aspx?schemecode=yhT+QBywfOQ=

There is none based on BSE 500 index.

Hope this helps.

hi Vipin … nice comparison , also i would like to add that having just 1-2 index funds in the markets is a bit of downer for investors. I had always wondered why there weren’t atleast index funds for major indices like midcap, bank, IT et al and then realized that some fund houses start thematic funds .. so in a vanguard like situation i would have multiple index funds to build my portfolio and then it will be a true comparison on whether actively managed funds beat the index funds .. can you please give your opinions on why there aren’t funds on more indices ? are the lower fees a bit of a dis incentive for fund houses to start them ?

Thanks for the comment Vikram. I guess lower fees isn’t the disincentive since the costs are lower too (no fund manager or research needed).

I guess, as of now, it is very easy to beat an index and hence active funds proliferate more than index funds.

I hope over time this should change.

Funny that I’m the only one commenting here, but I think we should benchmark mutual funds (whether actively or passively managed) against total return indices as suggested in http://www.thehindubusinessline.com/portfolio/your-money/give-the-dividend-its-due/article7855725.ece , https://www.valueresearchonline.com/story/h2_storyView.asp?str=28860 and http://www.arthvedacapital.com/wp-content/uploads/2014/03/Price-Vs-Total-Return-Index.pdf . The last link above says that only 30% of actively managed funds beat the total return index over any time period from 1 to 10 years. (Whether they beat index FUNDS is a different question.)

The aforelinked Value Research article also says that the market-cap-weighted index forces index funds to invest more in a sector that has a temporary rally, resulting in lower returns than an actively managed fund which can choose not to get carried away by the momentum. For example, Nifty and Sensex have 30% weight allocated to the financial sector. As the article says:

The NSE, for instance, now has a NSE Quality 30 (companies with most sustainable business models), CNX Alpha Index (50 stocks with the highest alpha), NV20 (20 companies that meet value criteria), which may be good benchmarks for active funds.

So, which index would you suggest using to measure my investment returns?

BTW, I suggest changing your comparison to compare active and passive funds that are benchmarked to the same index, not that have the same fund house. I think comparing a blue-chip fund with a CNX 500 index fund is apples and oranges. It would be better to pick an index, then pick 5 actively managed and 5 index funds that are benchmarked to that index, and compare them, irrespective of fund house.

Right Kartick, TRI is the correct measure to use. Yes, will definitely consider your suggestion. Thanks.

Regarding your point that HDFC Equity Fund isn’t performing well, I have an investment there. Should I exit it, waiting one year since the investment date to eliminate tax? Or is it okay to leave my investments there, but not make additional investments?

Or is the underperformance normal in the sense that good funds periodically underperform indices? If that’s the case, it’s okay to make additional investments in HDFC Equity Fund.

HDFC Equity is a great fund. Period. 🙂

Thanks so much for this. Data-driven analysis like you’ve done is much more reliable and scientific.

Thanks for reading and the appreciation. 🙂